1")

The Fed Reaches Neutral, What the December FOMC Meeting Means for Real Estate in 2026

Daniel Kaufman Real Estate

Federal Reserve Policy Research Note

December FOMC Meeting Analysis

December 12, 2025

Executive Summary

At its final meeting of 2025, the Federal Open Market Committee (FOMC) voted 9–3 to reduce the federal funds target rate by 25 basis points, bringing the benchmark range to 3.50%–3.75%. This marks the third consecutive rate cut of the current easing cycle and places overnight rates 175 basis points below the cycle peak.

The Federal Reserve’s updated Summary of Economic Projections (SEP) reflects a more constructive macro outlook, with lower projected inflation and stronger expected GDP growth through 2026. Chair Jerome Powell emphasized that policy rates are now “within a broad range of plausible estimates of neutral,” signaling a likely transition from active easing toward a more data-dependent pause.

For real estate investors, developers, and operators, this meeting reinforces a shift from rate volatility toward policy stability, albeit with growing internal debate within the Fed as labor market risks become more pronounced.

Policy Decision and Rate Outlook

The December decision lowered the federal funds rate to 3.50%–3.75%, continuing a gradual recalibration of monetary policy after an extended period of restrictive conditions. According to Chair Powell, current policy is now sufficiently balanced to allow the Fed to observe incoming economic data before determining the extent and timing of any further adjustments.

Importantly, Powell reiterated multiple times that the Fed views its current stance as near-neutral, positioning policymakers to respond flexibly should either inflation reaccelerate or labor market conditions deteriorate more quickly than expected.

From a capital markets perspective, this messaging reduces the probability of aggressive near-term easing while keeping the door open for incremental cuts should downside risks materialize.

Updated Economic Projections

The Fed’s quarterly Summary of Economic Projections provided several notable revisions:

Inflation: Projected to decline to 2.4% by the end of 2026, down from 2.6% in the September forecast. GDP Growth: Revised upward to 2.3%, compared to 1.8% previously.

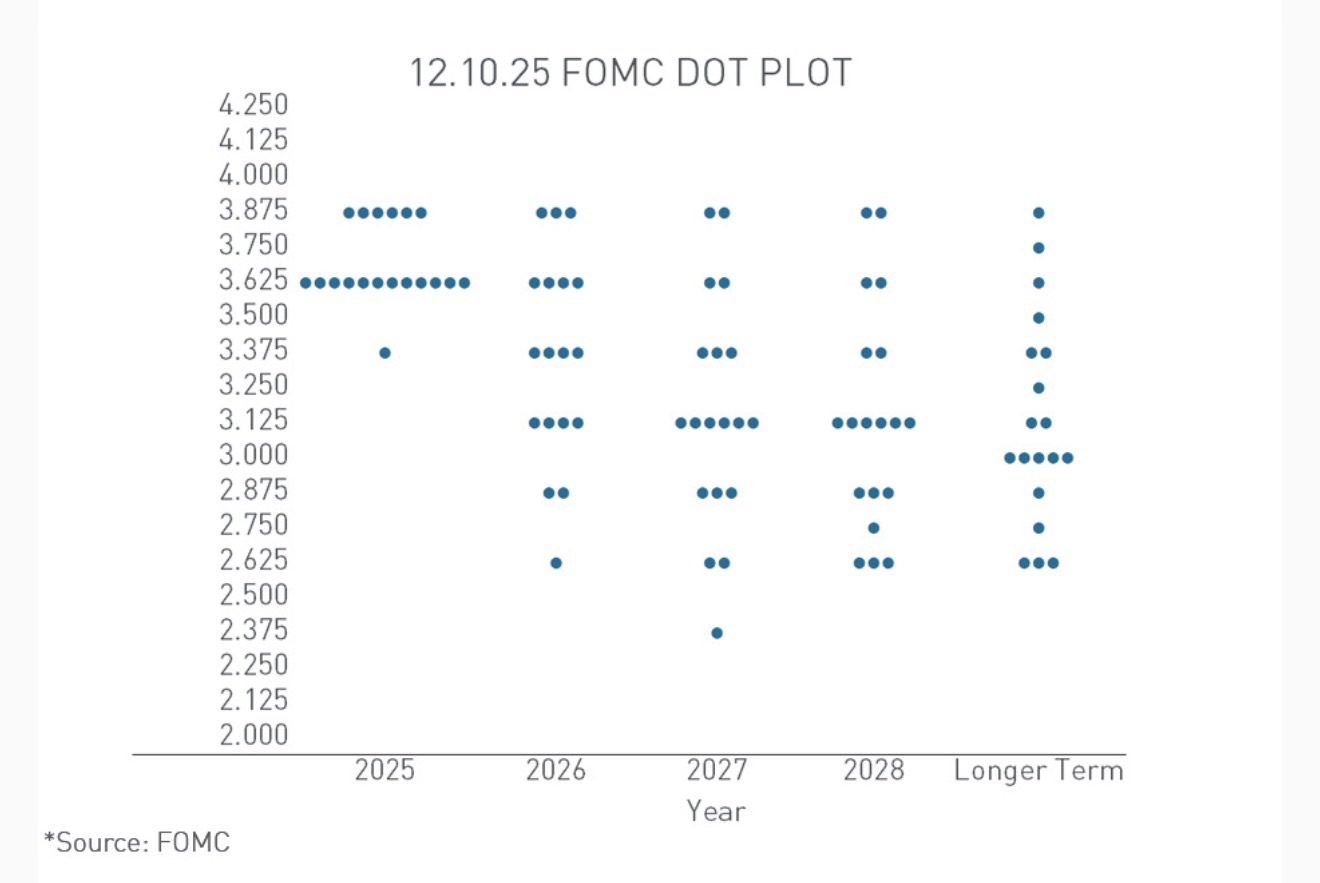

Rate Path (Dot Plot): The median projection continues to show one 25 bp cut in 2026 and another 25 bp cut in 2027, unchanged from prior guidance.

These revisions suggest the Fed sees an economy that is slowing modestly but remains fundamentally resilient, an important backdrop for real asset pricing, construction pipelines, and long-duration investment strategies.

Dissent and Internal Fed Dynamics

Three committee members dissented from the consensus decision:

Schmid and Goolsbee voted to hold rates steady. Miran dissented in favor of a larger 50 bp cut.

Chicago Fed President Austan Goolsbee, dissenting for the first time since joining the Fed in 2023, clarified that his objection was driven not by opposition to future cuts, but by a desire for additional inflation data before acting. In contrast, Miran’s dissent highlights growing concern among some policymakers that labor market softness may warrant a faster policy response.

Chair Powell addressed the dissents directly, noting that differing views reflect legitimate disagreements over the relative risks to inflation versus employment, rather than dysfunction within the committee. He emphasized that debate remains productive and that there is no single “risk-free” policy path at this stage of the cycle.

Labor Market and Data Constraints

The December meeting was held against the backdrop of limited new economic data, in part due to the recent government shutdown. Powell noted that available indicators show little change in the inflation or employment outlook since the prior meeting.

However, he acknowledged that recent labor market weakness appears driven by slower labor force growth combined with declining demand for workers, rather than acute economic contraction. This nuance is critical, particularly for labor-intensive sectors such as construction, development, and infrastructure.

Powell summarized the challenge succinctly:

“There is no risk-free path for policy as we navigate this tension between our employment and inflation goals.”

While consensus expectations lean toward a pause in early 2026, the Fed made clear that projections could shift quickly if labor conditions weaken further.

Implications for Real Estate and Investment Strategy

From the perspective of Daniel Kaufman Real Estate, the December FOMC meeting reinforces several key themes:

Cost of Capital: Rates appear to be stabilizing near neutral, improving underwriting visibility for acquisitions, refinancings, and development starts.

Construction and Labor: Persistent labor constraints remain a structural issue, particularly for housing and infrastructure, regardless of modest policy easing.

Asset Pricing: Lower inflation expectations support cap rate stability, though rent growth assumptions must remain conservative in a slowing economy.

Strategy: This is a market that rewards disciplined execution, patient capital, and projects aligned with durable demand drivers, including workforce housing, adaptive reuse, and infrastructure-adjacent real estate.

As we move into 2026, the Fed’s posture suggests fewer policy shocks, but also less reliance on monetary easing to drive growth. For real estate investors and developers, fundamentals, execution, and capital structure discipline will matter more than ever.

Daniel Kaufman

Daniel Kaufman Real Estate

Real Estate Development, Investment, and Market Research